|

Australian Suppliers Please Note:

FTNX Entrepreneurial Project Under Development

UPDATE Posted: 25 OCT 2024

ZERO EMISSIONS HUMAN ENERGY DEVICE:BIKE (ZEHED-BIKE) (ZED-BIKE)

Business: www.FTNX.net TRIBE Rules of Association www.ftnexporting.com

Visit to workshop by invitation only.Long read as such, mistakes/corrections applied in due course

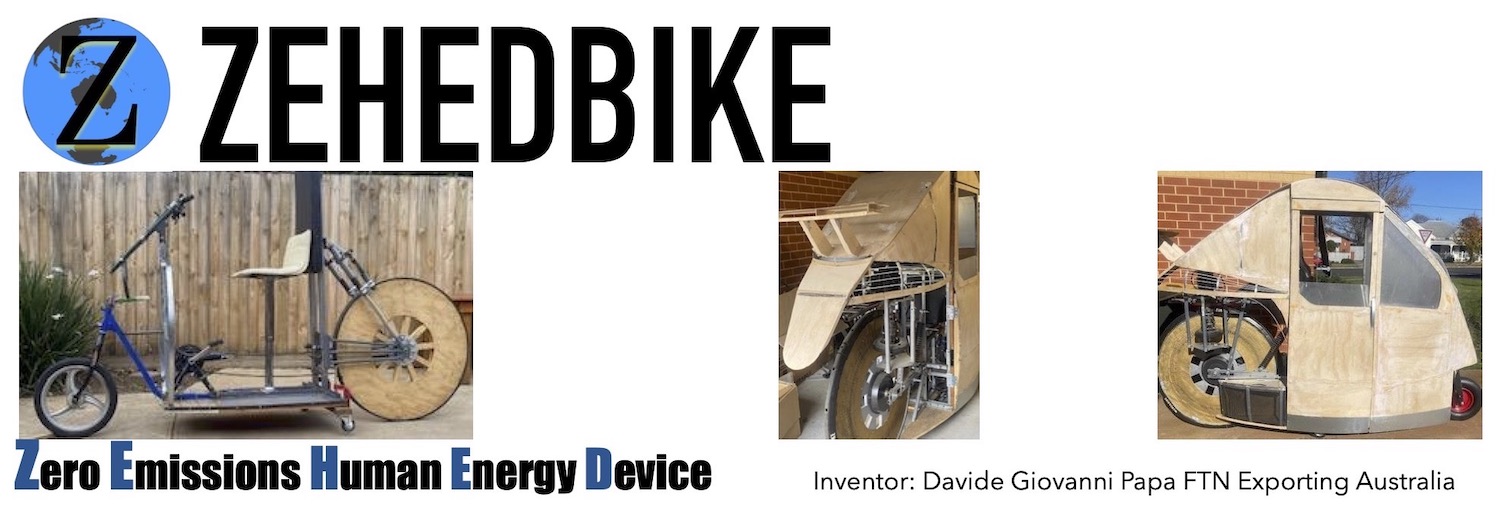

ZBike made by : Davide Giovanni Papa

Leading international best selling author and Inventor

ZEHEDBIKE

A two wheel covered ‘bicycle’ made for one person, allows us all to enjoy urban driving once more, with all the comforts of a car, without ever needing to buy emission laden fuel, batteries or use charging stations. The Human Transportation Pod (HTP) will be taking advantage of the power offered by the SUN in combination with human efforts made to drive the HTP. The very affordable all ‘peoples’ bike is the first unique standard model of its kind in the world, in this series. The ‘Aqua’ model will also float in places where flooded roadways are often evident. The second device is defined as ZEHED-AIR, which is another first, defined as a ZEHEDBIKE (ZED-BIKE) without wheels, as we eliminate another high carbon emitting product - synthetic rubber-tyres is also being developed once the original ZBike has commenced production.

To leave the car at home for short trips (or even longer trips) multiplied by 500,000 million users plus world wide will have a serious effect on mitigating carbon emissions.A major city having 10,000 ZBikes arriving and leaving every day affords the space usually needed to accommodate 20,000 cars. To mitigate emissions at the local level also delivers cleaner air locally in mitigating the harmful effect of current emissions produced by Ev’s and petrol cars. We need to start locally to arrest localised emissions and health issues, which in turn converts to national usage and subsequently international use. The ZBike will lead the way to cleaner air from a local perspective to a worldwide aspect, and aspect which current climate talks has not / cannot achieve the mitigation factors offered by the Zbike.

PREAMBLE

With the continuing success of “International Trade and the Successful Intermediary” (ITSI) FTN exporting has scaled down commodity trading to only consider large revolving contracts of NBC shipments, as we introduce ISPI. The publication ISPI will be our second formal publications describing intently once again, using actual experience, on how an informed intermediary could create an investment project and use the FTNX Beta Doctrine of Trade to create markets for the final product created via the final proposal initiated under an investment project. The PCT looking towards other entrepreneurial aspect of large international investment projects, can draw a wide inferences from ISPI, which will describe FTNX ZEHED-BIKE Investment Project in depth; to include aspects about creating the product and securing investment funds thereafter. As usual FTNX needs to first prove a concept personally before releasing a publication. It’s a huge technically challenging project, as such, smaller projects should also follow the same routine as applied in creating the Zehed-bike. “Just like the doctrine dogma states- always secure the product first; applies in matters of ISPI as well.”

ABOUT ZEHED-BIKE

The invention was fully created and prototype subsequently personally being built by FTN Exporting CEO and inventor Davide Giovanni Papa. From the first concept model to test the idea (Picture 1 above 2017: PIC 2, 2021: PIC 3, 2024) ) to the current 2024 aspect it has taken a long time to realise the concept. We are now 70% complete and will arrive at the fully operational beta prototype by late 2025. We’ll then test the ZBIKE for 3 month on real road conditions. “It all came about 13 years ago, while taking my usual daily walk in Melbourne city; so many people driving alone in such big cars, conducting many small trips daily. Too many big cars with one person in it , taking many short trips per day.” We are not interested in ‘fuel efficiency factors’ as the power of the Sun is free; and batteries are not needed . Reliability and longevity is our primary focus. Climate change is forcing the issue. “Sure, many who have followed my postings over the decades know, I don’t believe in climate change and the nonsense associated with such; but many do. This product will test the conviction of such people. In any case I do believe in the virtues of living on a planet with cleaner air.”

BUILDING THE ZBIKE FACTORY

Initial project will call for a plant employing 377 workers ( and 39 apprentices) harbouring various skill sets pertaining to carpentry as well as fitting and turning and metal fabrication, leather work, is being resurrected. We are unable to supply the world the required number of ZBikes, is already a known factor , hence the first plant is the model for other planets to be built overseas in accepted countries. The maths to date make this aspect viable while aiming to retain a net profit margin averaging 20% gross. Older work force with experience and ‘old school’ skills will be eagerly sought after . The flow on effect into the supply chain and export strings as well as local retail sales will generate thousand of added jobs by default. Finished product to be sold internationally at first in conjunction with selected FTNX SPCT agents (FTNX will consign supply to selected and capable territorial agents) as FTN Exporting is already a leader is the matter of exports. ZEHED BIKE will become owned by FTN Exporting in 2026. FTNX will handle all matters of exporting the ZBike. The first factory production line will be established in Bacchus Marsh, Victoria, Australia, subject to government assistance.If the Victorian Government will not assist other states will be approached. Workers will be paid for a full 5 day 40 hour week while only working a 4 day 35 hour shift on the condition no public holiday rates are paid ( yet to be raised with relevant unions). This aspect will allow the factory to remain open 365 days per week. Well paid less stressed workers , will often increase productivity and besides all benefits paid, workers have 5.0% production bonus of sales set aside as well. Worker employed by ZB must feel a personal connection to the hand made product they are helping to build. ZBIKE prototype is nearing completion with final certified road testing to take place in late 2025. A new website will be incepted at this time dedicated to matters of the ZEHED-BIKE. No products from China or India will be considered as the aim is to produce a high quality product locally and revive past manufacturing aspects which were once common in Australia; without relying on the use of products from China or India. Franchised manufacturers world wide will also need to comply with the same aspect. The ZBIKE has to be made locally using locally sourced material.

ABOUT THE ‘ZEHED-BIKE’

A fully covered self charging 2 wheeled ‘bike’ ( built sturdy like a car) weight over 200 kilograms, except it has foot peddles that requires 40% human energy and 60% solar/light energy to produce 100 percent efficiency without any emissions being produced. No batteries are used to feed the 12 Volt 250 Watt 30 amp electric ‘capacitor motor’ ( another first). As already tested, one full crank of the ZBIKE peddle delivers a unique travel distance of 3.12 metres. Solar energy is collected and ‘stored’ to power its 250 watt electric motor in large can capacitors that will hold the required 30 seconds worth of useable current until used, with a recharge time of 5 seconds once capacitor are depleted. “It’s like carrying pure electricity in a suitcase without the heavy costly aspects of storing large dirty batteries.” The Zbike is not a ‘Pedelec’ type of bike. Standard features include, ZBike to ZBike line of sight communication, radio, UV virus filtrations (to kill viruses entering the Pod) side windows, full dash and instrumentation, using a combination of buttons, switches as well as LED components, reverse, 2 doors/widows, disc brakes, air con, heater, indicator lights, phone charger, seat belt, medium range radiation insulation, speakers, and even a coffee cup holder.etc.etc. There is ‘no excuse’ to take the car for short trips. When no Sun is available, peddling backwards while coasting forward will charge the capacitor in under 5 seconds takes care of night time or cloudy day driving. Two pilot wheels are lowered to steady the ZBike when not moving, to steady the ZBike until it attains a speed of 5 KPH or less. ZBike trunk can carry an added 12 kilos (ideal for shopping). No gears are required as a special feature of its drive allows for torque to match the speed of the unique oversized ‘Chariot’ style back wheel. The purpose of the ZBIKE is designed to eliminate the use of the petrol car for short trips, where at peak times often ‘one person’ is seen driving such petrol /battery /hydrogen fuelled cars, suited to carry 4 people at short distances is not conducive to matters of curbing carbon emissions.This is the issue regardless what type of car is driven. Many people driving short distances in a vehicle designed to do a lot more other than polluting the air. The ZBike will make driving fun once more.’ A ZBIKE is designed for lifetime use, where spare parts and ease of replacing parts plays its ‘part’ in reducing carbon emission as the cost of ‘recycling’ products often cost more and produces more emission than when the product was made. A return trip distance totalling 20 kilometres is considered a ‘short trip.’

ALL PEOPLE’S VEHICLE

Planned obsolescence is now a thing of the past. Long lasting reliable products are now the focus of future manufacturing basis world wide. Only a hand full of specialised parts will need to purchased where /if repairs are needed. ZBike will be able to reach high speeds but will be restricted to not go beyond 45 KPH when under power in Australia as speed limits on bikes and the wearing of helmet may still apply until the popularity of the ZBike become notable. All such limitation are lifted depending in where the Zbikes are exported to as such, bigger motors will be available in certain countries. The ZBIKE is made for everyone to use for local suburban driving situations (including, paramedic, heated food delivery, amphibian and police supercharged 600/750 watt models are envisaged) Currently the ZBike will be offered at the affordable FIXED WORLD WIDE delivered export price of around USD$ 3700.00 (2022/23 basis) for the basic standard model and USD$ 4900.00 for the executive model. A uniform standard world wide retail export price will establish the ZEHEDBIKE as a valuable re-sellable commodity is again another FTN Exporting initiative. One price basis world wide fully delivered include all freight costs is a never tried before concept. Licence to manufacture ZBikes in other states and countries will be offered once the incepting factory proves viability, as the need and demand for this kind of transport system will be great for many decades as climate change rhetoric escalates. Even Nordic countries where yearly availability of sunlight is diminished, varying complimentary 12 Volt standard no lithium battery connection sockets will be included to ensure longer period of clean sustained driving in colder climates, may be utilised as needed, to compliment the human energy aspect, using almost any kind of batteries on hand ( connecting a car battery - or even easy to buy and replace D size batteries is a simple process.) Even an input is also included to fit common over the counter 18 to 24 volt / 5.0Ah power tool battery to assist with lights and heating in very cold countries. The ZBIKE is built using the principle of “over compensation” in where each part used greatly exceeds international minimum standards. This aspect will ensure the longevity status of the ZBike. Electronics components are not needed as we return to the reliable aspect of analog technology. The weight of the ZBike is an important factor as a ‘heavier’ and stronger the ‘bike’ is, adds to the overall claims of reliability made. Without the burden of using a large battery, weight is added to the frame to make it very strong. Parts when needed, will be inexpensive and repairs, can easily be done by most ‘hands on people,’ is also an added unseen feature. A hardware store will be able to supply most replacement parts. The ZBike will have anti theft devices fitted as well. “ Nobody with throw a ZBike away-ever, as they become an important asset for people to use.” Blank unpainted models are also available for budding artist to add their own artwork to the parts of the body not covered by solar panels. Organic naturals paints will apply to all ZBikes painted at the factory.The factory itself will also have its own solar/energy farm, to compliment the energy used to make the ZBikes.

INVESTMENT POTENTIAL

Initial plan of attack is as follows, which may change when the the prototype is fully operational and tested intently. FTNX will initiate the final prototype and prove the concept supported by a business plan. FTNX will then seek funds to finance the project currently estimated to be US$ 39 ,000,000.000; defines the investment capital sought to fund the project bearing a 50% share capacity. Initial listing of share will carry a nominal value starting at US$0.20 cents up to US$ 2.00 per unit . Local and federal government will also be approached to serve part of this investment. ZBIKE will become profitable within 26 months of operations commencing. Entering the export market is already assured via FTN exporting with informed SPCT members being approached to act as our Agents in countries where ZBIKE plants are to be built. Initially 1,000 ZBikes to be built per week in the Australian plant is being planned, where maximum production capabilities to be arrived at by the end of the initial 26 months of commencing operations. Other ZEHED devices are also planned under a R&D aspect. Once operational aspect are completed, ZBIKE plant license will be served for Zbikes to be built Internationally in Europe , Canada, London, USA, Japan and possibly a few others, as per the Australian operational blueprint. One plant in Australia will not be able to supply world markets even if efforts to provide supply is applied over a 25 year period and beyond. We estimate that on a grand scale over the next 25 years, ZBike sales alone will exceed 500,000 million units, without considering other ZEHED-Industry inspired products and concepts, which are many. Even if only a third of the production estimates eventuate–a trillion dollars worth of sale would be achieved. The scope and investment potential is huge. FTNX will prove concept, and secure a plant and establish the operational aspect. Investors take a stake the project by financially supporting it at inception.

USING THE ZBIKE

You have parked your Zbike outside which is already lapping up the morning sun. The excess energy will automatically either cool the cabin down or heat it up depending on the outside temperature. The Zbike is sitting on two retractable pilot wheels.You enter the cabin by opening the door. Their seat is taken, seat lap belt is applied (option). Steering arm is gripped firmly in hand. The driver must peddle first to get the Zbike travelling at 5 KPH or more. This is very important as the need for large batteries is mitigated by the fact that human energy is used when the most power is needed- at takeoff. The Zbike is designed to peddle at this speed effortlessly. At 5 KPH press the throttle on the steering arm half way and the Zbike will take off. If the sun is partly covered by clouds, gently peddling backwards will also charge the bike in seconds while the Zbike is coasting. As the Zbike picks up speed, let go of the throttle to coast the ZBIKE, within seconds the Zbike is again fully charged able to supply 30 seconds of direct power as needed. The ZBike has a massive rear wheel and rear bearing made for coasting. Once a clear path is apparent, press the throttle all the way down; at maximum power for 30 seconds the Zbike will pick up to reach speeds of in access of 40 KPH quickly. If the road is long, let go of the throttle so that the Zbike coasts e.g at 40 Kph; it will then take 5 seconds to recharge the Zbike with another 30 seconds worth of stored energy. With this process especially on full Sunny days the Zbike could cover vast distances and reach high speeds. At night time the same process applies except now there is no sunlight, therefore by peddling backwards for 3 or 4 seconds , the bike becomes charged for 30 seconds. If it’s raining– wipers are fitted. If it’s cold, a heater is available. If it’s very hot, the unique ZBike air conditioner may be switched on. When on the road, with other ZBike commuters, the ZBIKE communicator allows a Zbike driver up to 50 metres always to advise other drivers by speaking in the cabin. Drivers behind hearing of any adverse driving situations encountered and visa versa, can take an alternate route; creating an informed ZBike community. E.g: “ZBike 007 mains street blocked ahead due to crash, police have closed the road… take alternative route..etc..etc.” The Zbike Com can be turned off or on at will. Breaking is applied by moving the steering arm forward. The more forward it is pushed, the more breaking is applied. Zbike uses solid rubber tyres for now; which means no flat tyres. We are working on future wheel design to eliminate using rubber on the wheel to usher in a new epoch where tyres are not longer needed( Via ZEHED AIR will also be developed once the plant is established) Parking is done nose out is best practice. If you do get stuck ‘nose in’ where reverse is needed, a switch allows the ZBike to pulsate reverse current to the back wheels– to allow slow reversing application. Steering is road direct. The driver ‘feels’ the road intently all times especially when hugging corners. Air entering into the cabin must pass UVC light and pollen filters. It must also pass UVC light on the way out; making the cabin a 99.0% virus free environment. Series II ‘Aqua’ model, will also be able to cross still flood waters. Very steep hills are tackled by traveling up such hills in a zig zag manner, by using corresponding side streets. Series I will come with very strong 6 mm acrylic windows. Series II will come with harden glass screens as we eliminate further carbon emitting products and footprints therein. Interior will use mostly wool, cotton, calf and rabbit skins.Where allowed, larger motor and even things like a Defibrillator (medical services) or hot food delivery heated compartment can be added as the Zbike can carry an access weight of between 15 and 25 kilograms. Police mall/laneway patrols can also be conducted with Zbike as provisions such as handcuff railing can be incorporated. While powering and coasting the Zbike initial test have easily reached 60 kph, as such the Zbike will have speed limiter applied when exported to some countries. The ZBike has electronic locking and anti theft devices which cannot be ‘hot-wired’ as well as a micro spotted frame with details to identify the Zbike a with its owner is incorporated. Iphone charger, a bluetooth ZBIKE app, and a cup holder are included. A large led light dash showing power consumption and speedometer.etc.etc is also fitted as are night lights and turning indicators. Input for e.g: hairdryer, shavers, suit case/coat / bag holder etc.. also included. Should the motorised aspect unlikely break down; a “get you home” peddle mode is available as is a front towing bar. All the comforts of a car, now serves reason to leave the car at home to favour the Zbike when taking short trips- with no fuel cost. For long trips and ‘adventures’ electrical output on the outside of the cabin ( e.g: when camping ) is also available as the peddle generator is able to produce up to 22 volts when peddling backwards while at standstill. Countries where helmets must be worn (not many) when riding a bike, ( hopefully such laws will be removed for Zbikes in Australia ) a head rail is fitted, so that the Zbike helmet can remain attached to such after the drivers exits. The pilot wheels remain down and are mechanically lifted automatically once the throttle is activated at 5 KPH or more. A loss of power means the pilot wheels remain down. Two compressed air- air bags , fill the cabin in the event of a serious accident.

Next Update advised when Zbike is ready for road testing in 2025.

Disclaimer

No investment capital is currently being sought with the release of information pertaining to the development of the ZEHEDBIKE. FTN Exporting CEO Davide Giovanni Papa is personally developing an investment project the details of which will be published in “International Projects and the Successful Intermediary” (IPSI) in 2026. ISPI is made to compliment our current mainstream doctrine (ITSI). ITSI and ISPI together will provide the insight on how an informed PCT can also create an low capital investment project within 5 years or less. As usual, FTNX only release a publication after its basis has been vigorously tested first.Information offered herein is done so as current at the time of disclosure without revealing key aspects or disguising actual components that will officially be used, as a matter of secrecy in protecting aspects of such key components. Over time the information offered ‘today’ may change to deliver the final concept by 2026.The operational aspects offered are correctly asserted at time of writing.

|